A Multi-Part Series

The stock market just gave us a reminder of what volatility feels like.

I’m writing on the day following a two-day, 8% plummet in the Dow Jones average. Everyone I talk to asked, “What happened?” “What do I do?” “Will it get worse?”

The most frantic questioners were those who had the largest amount of their savings in stocks, especially the ones who depend on equities to provide them with their retirement cash flow. (Even the Millennials got spooked when their robo-advisors jammed up.)

The pundits immediately suggested that investors “stay the course.” Some also opined, “This market correction probably was a good thing.”

But think about the investor whose cash flow depends on the value of the market, someone who takes required minimum distributions from her 401(k) or rollover IRA. She just experienced serious “Income Volatility” – a reduction in income from a fall in the market. It was the last thing she needed.

Income allocation over asset allocation

I believe we can create income allocation strategies that don’t collapse with our confidence when the market goes haywire — and that can reduce income volatility to near zero.

Here is a rough illustration of my own situation, which allowed my wife and me to stay calm during the drop. I concentrate on income allocation and the minimization of income volatility, not asset allocation and market volatility. And the plan is to provide income for the rest of our lives, however long it might be.

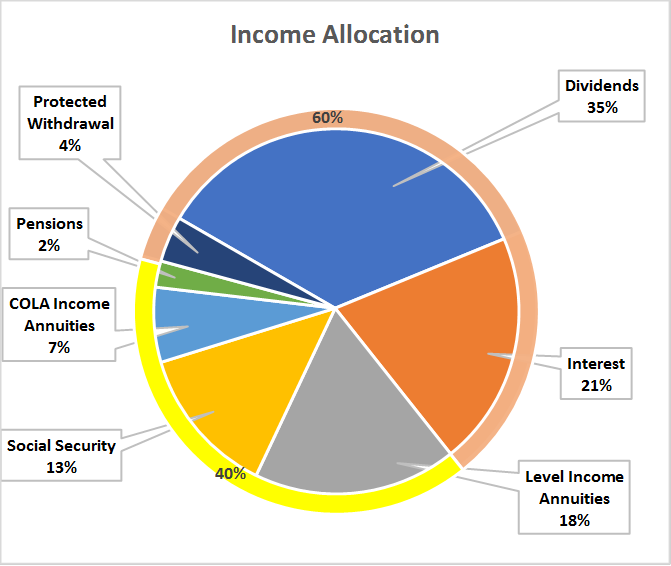

The pie chart shows where my income comes from. Note that a high percentage of this income is likely to grow, addressing most of my concerns about inflation. If you add in my life insurance, long-term care insurance and longevity insurance in the form of a deferred income annuity called a QLAC, my plan is protected from life risks. Not everyone can get to a plan like this but it’s worth striving for.

How did I get to this position?

How did I get to this position?

As an investment advisor, I understand the power of high-dividend stock portfolios and ways to manage income volatility.

As a retirement income planner, I understand the difference between income and withdrawals. (When your plan is set up correctly, it means that today’s cash flow doesn’t impact future income.)

As an actuary, I appreciate and understand the unique benefits that life insurance, long-term care insurance and income annuities can provide.

And as a fellow Boomer and consumer of financial products, I understand the peace of mind I get from regular “paychecks” – along with the pleasure of seeing as little as possible go out in taxes.

While my background gives me a particular advantage, there’s one thing that all investors and their advisors can do for us Boomers: Think of the plans you’re building for retirement as being not about “asset allocation,” but about “income allocation.” The goal is to minimize income volatility.

Parts II and III of this series give you background on why and how an income allocation plan can work for you.

Jerry Golden is the founder and CEO of Golden Retirement Advisors Inc. He specializes in helping consumers create retirement plans that provide income that cannot be outlived. Find out more at Go2income.com, where consumers can explore all types of income annuity options, anonymously and at no cost.

Earn up to 20 percent more in retirement with income allocation strategy

[…] strategy of asset allocation, and delivers that additional income with less risk. Here’s a good description of the income allocation […]

Do you have enough income to retire? Switch to income allocation

[…] Parts I and II in this series, I suggested that you could receive more retirement income with less […]

Asset allocation answers: Do I have enough money to retire?

[…] Part I of this series on asset allocation, we examined the difference between asset allocation and income […]