Right now, inflation is top of mind for everyone, including retirees.

Inflation is important. But it is only one of the risks that retirees have to plan for and manage. And like the other risks you have to manage, you can build an income plan so that rising costs (both actual and feared) do not ruin your retirement.

Inflation and Your Budget

Remember that in retirement your budget is different than when you were working, so you will be impacted in different ways. And, of course, when you were working your salary and bonuses might have gone up with inflation, which helped offset long-term cost increases.

Much of your pre-retirement budget was spent on housing — an average of 30% to 40%. Retirees with smaller or paid-off mortgages will have lower housing costs even as their children are busy taking out loans to buy houses, and even home equity loans to pay for home improvements.

On the other hand, while health care looms as a big cost for everyone, for retirees these expenses can increase faster than income. John Wasik recently wrote an article for The New York Times that cited a recent study showing increases in Medicare Part B premiums alone will eat up a large part of the recent 5.9% cost of living increase in Social Security benefits. As Wasik wrote, “It’s difficult to keep up with the real cost of health care in retirement unless you plan ahead.”

Inflation and Your Sources of Income

To protect yourself in retirement means (A) creating an income plan that anticipates inflation over many years and (B) allowing yourself to adjust for inflation spikes that may affect your short-term budget.

First, when creating your income plan, it’s important to look at your sources of income to see how they respond directly or indirectly to inflation.

- Some income sources weather inflation quite well. Social Security benefits, once elected, increase with the CPI. And some retirees are fortunate enough to have a pension that provides some inflation protection.

- Dividends from stocks in high-dividend portfolios have grown over time at rates that compare favorably with long-term inflation.

- Interest payments from fixed-income securities, when invested long-term, have a fixed rate of return. But there are also TIPS bonds issued by the government that come with inflation protection.

- Annuity payments from lifetime income annuities are generally fixed, which makes them vulnerable to inflation. Although there are annuities available that allow for increasing payments to combat inflation.

- Withdrawals from a rollover IRA account are variable and must meet RMD requirements, which do not track inflation. The key in a plan for retirement income, however, is that withdrawals can make up any inflation deficit. In Go2Income planning, the IRA is invested in a balanced portfolio of growth stocks and fixed income securities. While the returns will fluctuate, the long-term objective is to have a return that exceeds inflation.

- Drawdowns from the equity in your house, which can be generated through various types of equity extraction vehicles, can be set by you either as level or increasing amounts. Use of these resources should be limited as a percentage of equity in the residence.

The challenge is that with these multiple sources of income, how do you create a plan that protects you against the inflation risk — as well as other retirement risks?

Key Risks That a Retirement Income Plan Should Address

A good plan for income in retirement considers the many risks we face as we age. Those include:

- Longevity risk. To help reduce the risk of outliving your savings, Social Security, pension income and annuity payments provide guaranteed income for life and become the foundation of your plan. As one example, you should be smart about your decision on when and how to claim your Social Security benefit in order to maximize it.

- Market risk. While occasional “corrections” in financial markets grab headlines and are cause for concern, you can manage your income plan by reducing your income’s dependence on these returns. By having a large percentage of your income safe and less dependent on current market returns, and by replanning periodically, you are pushing a significant part of the market risk (and reward) to your legacy. In other words, the kids may receive a legacy that reflects in part a down market, which can recover during their lifetimes.

- Inflation risk. While a portion of every retiree’s income should be for their lifetime and less dependent on market returns, you need to build in an explicit margin for inflation risk on your total income. The easiest way to do that is to accept lower income at the start. For example, under a Go2Income plan, our typical investor (a female, age 70 with $2 million of savings, of which 50% is in a rollover IRA) can plan on starting income of $114,000 per year under a 1% inflation assumption. It would be reduced to $103,000 under a 2% assumption.

So, what factors should you consider in making that critical assumption about how much inflation you need to account for in your plan?

Picking a Long-Term Assumed Inflation Rate

Financial writers often talk about the magic of compound interest; in real numbers, it translates to $1,000 growing at 3% a year for 30 years to reach $2,428. Sounds good when you’re saving or investing. But what about when you’re spending? The purchase that today costs $1,000 could cost $2,428 in 30 years if inflation were 3% a year.

When you design your plan, what rate of inflation do you assume? Here are some possible options (Hint: One option is better than the others):

- Assume the current inflation of 5.9% is going to continue forever.

- Assume your investments will grow faster than inflation, whatever the level.

- Assume a reasonable long-term rate for inflation, just like you do for your other assumptions.

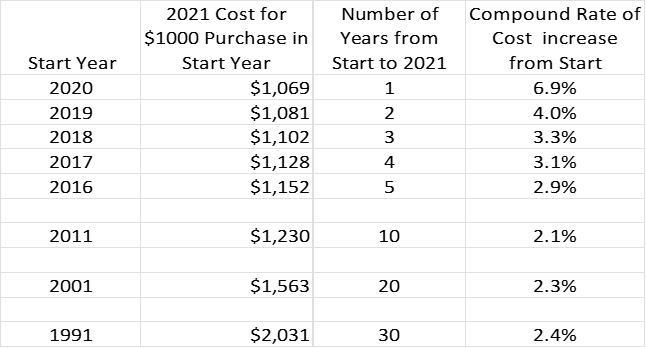

We like the third choice, particularly when you consider the chart below. Despite the dramatically high rate of today’s inflation that affects every result in the chart, the long-term inflation rate over the past 30 years was 2.4%. For the past 10 years, it was even lower at 2.1%.

A Long-Term View Smooths Inflation Spikes

Managing Inflation in Real-Time

Whether you build your plan around 2.0%, 2.5% or even 3.0%, it is helpful to realize that any short-term inflation rate will not match your plan assumption. My view is that you can adjust to this short-term inflation in multiple ways.

- Where possible, defer purchases that are affected by temporary price hikes.

- Where you can’t defer purchases, use your liquid savings accounts to purchase the items, and avoid drawing down from your retirement savings.

- If you believe price hikes will continue, revise your inflation assumption and create a new plan. Of course, monitor your plan on a regular basis.

Inflation as Part of the Planning Process

Go2Income planning attempts to simplify the planning for inflation and all retirement risks:

- Set a long-term assumption as to the inflation level that you’re comfortable with.

- Create a plan that lasts a lifetime by integrating annuity payments.

- Generate dividend and interest yields from your personal savings, and avoid capital withdrawals.

- Use rollover IRA withdrawals from a balanced portfolio to meet your inflation-protected income goal.

- Manage your plan in real time and make adjustments to your plan when necessary.

You can put together a plan at Go2Income here and also modify it by adjusting your expectations and investments. You may also ask for help from a qualified advisor who can answer questions and assist in navigating the process.

Inflation is a worry for everyone, whether you are retired or about to retire. Put together a plan at Go2Income and then adjust it based on your expectations and investments. We will help you create the best approach to inflation and all retirement risks you may face.