A savvy consultant recently asked me how much more income a Go2Income plan, with its integration of annuity payments and focus on income allocation, could produce as compared to a traditional retirement income plan. Might it be 20% or more?

He recalled my discussion about rules of thumb in Retirement Planning: One Size Doesn’t Fit All. In that article, I pointed out that the Starting Income Percentage (SIP) for a Go2Income plan was 5% — vs. the “4% rule of thumb” many advisers include in their plans. (That extra percentage point, from 4% to 5%, is a 25% gain.)

But I couldn’t give that consultant a definitive answer or a single percentage — because each investor is different. Investors will:

- Bring a unique profile based on age/gender/marital status and savings.

- Have a different set of retirement objectives and tolerance for risk.

- Experience a particular set of market results.

So, while I believe in Go2Income planning, I am ducking the “income advantage” question until we discuss the numbers question in more depth.

It’s Not All About the Numbers

In designing the Go2Income planning method and process, reducing the “risk of ruin” — or running out of money in retirement — is our No. 1 objective. And within that constraint, the method strives to achieve the investor’s legacy objective wherever possible.

Assembling and presenting the numbers so that an investor can understand the plan and what the numbers mean is critically important. Here’s our process:

- To introduce a plan to an investor, we deliver a “starter” plan focusing on a few key plan results: starting income, annual percentage increase in income to age 85, percentage of safe income and legacy at 95.

- To present the detail, we use plenty of illustrated graphs to show investors the plan in an easy-to-digest form. Some examples are below.

- To capture the often-conflicting objectives of income and legacy, we use a “decision table” that helps us compare plans on a more scientific basis.

Set out below are illustrations of these three steps.

1. Simple Definition of Plan

Here’s how we describe a starter Go2Income plan for the investor we often use in our examples (a 70-year-old female with $2 million in retirement savings). Her starting income in the Go2Income plan is $114,000 per year, and it will grow by 2% a year to $135,000 at age 85. About 60% is safe, meaning it’s not coming from the sale of investments. Her legacy at age 95 is $2,730,000 as she reinvests her income in excess of her 5% income goal of $100,000 per year. We’ll use this example for the balance of the article.

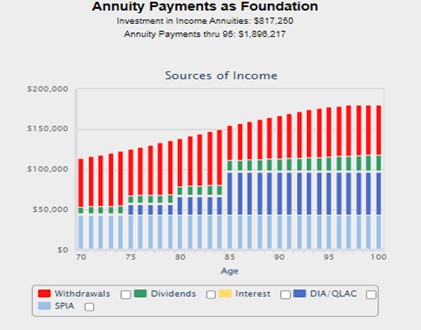

2. Capture Details in Easy-to-Digest Graphs

The projected results of every decision you make can be explained clearly and quickly in a visual way, often with a graph. Such visual aids will also show how unexpected turmoil — inflation, recession — might affect your income stream. For the case above, here’s how graphs fill in the picture:

Sources and Projection of Income

Sources and Projection of Legacy

3. Considering Plan Income, Income Goal and Legacy

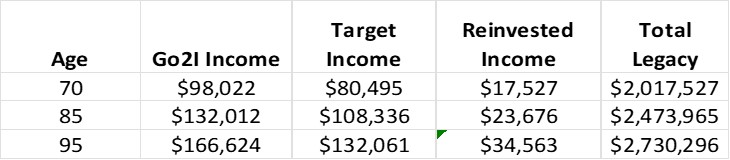

The above graphs and starter plan information look at income and legacy separately. But how do you achieve both sets of objectives? We had to develop a “decision table” like the one below, which shows the following:

- Income from a Go2Income plan based

on a set of planning assumptions.

- Target income set by client; in this case, 5% of savings, growing by 2% a year.

- Excess income available to reinvest, or liquidate if there is a deficit.

- Legacy from the Go2Income plan together with the value of reinvested or liquidated income.

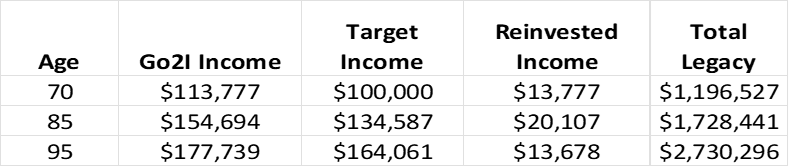

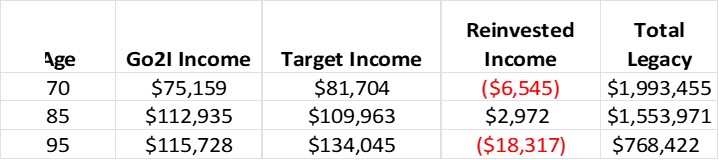

Here’s our decision table for the plan adopted by the investor based on an 8% long-term stock market return (after fees) and other standard assumptions.

Go2Income Plan with 8% Long-Term Stock Market Outlook

This plan seems to work out, since our investor is meeting her target income and reaching a legacy in excess of her initial savings, but that’s not true in every situation. Let’s use our decision table tool to answer the most frequently asked and fundamental questions.

Frequent Questions About the Plan

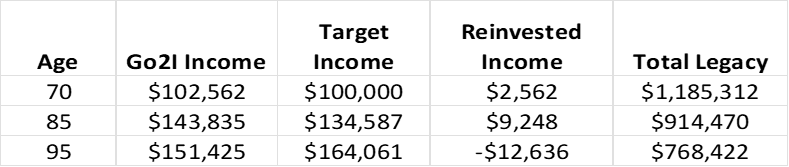

Q: What if the market doesn’t achieve a long-term 8% stock market return and does only 4% over the long term?

Using this same set of measures, the plan illustrated below still meets the income objective, but delivers a lower legacy at 95 of $768,000. Under Go2Income, most of the market underperformance has been pushed to the kids or grandkids.

Go2Income Plan With 4% Long-Term Stock Market Outlook

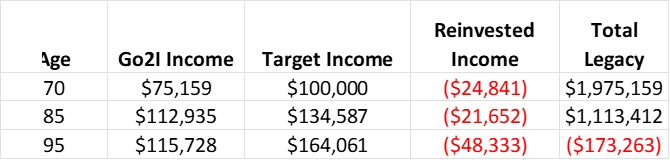

Q: What if I get rid of annuity payments and achieve the same 4% long-term performance?

Rather than ending with $768,000, the legacy portion of this plan runs out of money by age 92 — primarily because there’s no source of income, like annuity payments, that is unaffected by the market.

Go2Income Plan With 4% SMO and Without Annuity Payments

That’s not a satisfactory result.

What’s the percentage advantage “number” for these two scenarios?

Getting back to the consultant’s question, our analysis does show a large bump in the income goal while meeting a long-term legacy objective by using Go2Income.

Here’s the way I would describe that increase:

- If you believe in a long-term return on the stock market of 4%, but don’t want to include annuity payments, then to match the Go2I legacy at 95 (and to avoid running out of money), you’ll have to lower your goal from 5.00% to 4.09%.

Go2Income Plan With 4% SMO, Without Annuity Payments and 4.09% SIP

- If you believe in a long-term return on the stock market of 8% and want to eliminate annuity payments, then to match the Go2Income plan’s legacy at 95, you’ll have to lower your goal from 5.00% to 4.02%.

Go2Income Plan With 8% SMO, Without Annuities and 4.02% SIP

Depending on how you look at it, adding annuity payments and using the decision table, there’s a 22% to 25% increase in income.

That’s impressive. And although your situation will be different, a Go2Income plan is designed to create more income and long-term legacy. For everyone.

When you are ready to discuss a retirement income plan that allows you to enjoy the rest of your life without big money worries, go to our landing page, answer a few simple questions and begin to create your plan.