50% of Retirees will Incur Long-Term Care Costs: Stay in Your Home and Let’s Pay Those Costs

It’s more than just longevity protection. It’s about the option to age-in-place. To be able to help kids and grandkids now and when you pass. And no compromises on care.

For most of my life, I’ve worked as an innovator in the financial services space, with a particular focus on life insurance and annuity products. For 40 years, that was my job and specialty. One of my “first of a kind” product inventions — the Accumulator — offered downside protection on the income that a variable annuity could provide and eventually created a $1 trillion industry.

In my current role as an investment advisor focused on retirement planning, my innovations address the current needs of retirees regarding greater longevity, concern about Social Security, high inflation, taxes and increasing medical and long-term care costs. As this survey of retirees by Schroders details, those are the top concerns of many people in retirement.

The concerns about costs of long-term care are about to increase, with a new federal Medicaid rule that, beginning in 2028, will cap allowable home equity at $1 million. This will most directly affect middle-class homeowners in high-cost markets. Under current rules, states set the amount of equity that a homeowner could maintain and still qualify for Medicaid LTC coverage. It ranged from about $750,000 to $1.13 million — and it was adjusted every year for inflation. In 2028, the allowable equity will be $1 million for everyone (except farm families) and it will not be inflation indexed. Of course, there are other related costs that Medicaid will not cover, like assisted living or for services like a home aide, unless the retiree satisfies means test.

Change in retirement planning is necessary

As it happens, I’ve been working on a new design for retirement planning that addresses long-term care costs. It does require, among other things, a breakdown of the silos between investments, annuities and housing wealth.

This design change doesn’t focus on the wealthy or lower-income retirees, but rather the broad group of so-called mass affluent. The most popular planning approach for this group of retirees is to invest in different investment portfolios and withdraw 4% to 5% per year, increasing by inflation. Intuitively, most retirees know that they can do a lot better not only in the level of income, but also in the reduction of risk and taxes, and in greater liquid savings.

On the other hand, most don’t fully appreciate the potential costs of long-term care. Not surprisingly, those who live longer are more likely to need long-term support and services like nursing home care. One interesting statistic is that 50% of retirees age 85 and over will need long-term-care services, which are in the $80,000 to $150,000 per year range, with a historical increase rate of 3% to 5% per year, with a higher rate of increase post-COVID.

Our analysis suggests these costs will represent nearly 25% of the average $2 million in net worth split between a Rollover IRA and value of house. Without planning for those costs in advance, the sale of the house may be required.

Here are the retirement planning design changes we developed.

Consider all major asset classes — include housing wealth and lifetime annuities

In figuring out a solution to these retirement challenges, whether or not Medicaid is an option, it made sense to look at all of a client’s net worth. That struck a chord when housing wealth was reported as 50% of our sample retired client’s wealth. Importantly, the innovations needed to be doable with no regulatory change or product refinement — and simply in the retirement planning space. It had to be accomplished through our planning algorithm and executed by an advisor through partnering with different product providers.

The first step was how to include housing wealth in the planning. The second was the integration of the most logical but underutilized retirement product — lifetime annuities. The key for me was to consider them together rather than separately. Why together? It answers the following key objections (See Transform Your Retirement Plan ) that often are raised about each product individually:

- Housing Wealth — If using a reverse mortgage such as a Home Equity Conversion Mortgage (HECM) to unlock this wealth, the objections are the costs and risks if you borrow too much. Read How Your home Can Fill Gaps In Your Retirement Plan.

- Lifetime Annuities — A Qualifying Longevity Annuity Contract, or QLAC, can help define a better retirement by deferring taxable IRA distributions and delivering guaranteed lifetime income at an age you select. Read A QLAC does So Much More Than Simply Defer Taxes. Despite a lifetime payout for a 67-year-old male of, say, $50,000 per year on a $100,000 premium, retirees often object to the lack of liquidity.

In our development phase, we said “HECM meet QLAC.” Individually, both HECM and QLAC can be helpful in their own ways. Together, we call it HomeEquity2Income, and the combination can help you stay in your home as you build liquidity for possible long-term care costs, as well as boost income. It also means you don’t have to spend down the savings in your Rollover IRA to qualify for Medicaid.

Here’s how we put them together:

- Set up a line of credit through HECM and purchase QLAC from Rollover IRA savings

Housing Wealth – HECM Rollover IRA – QLAC

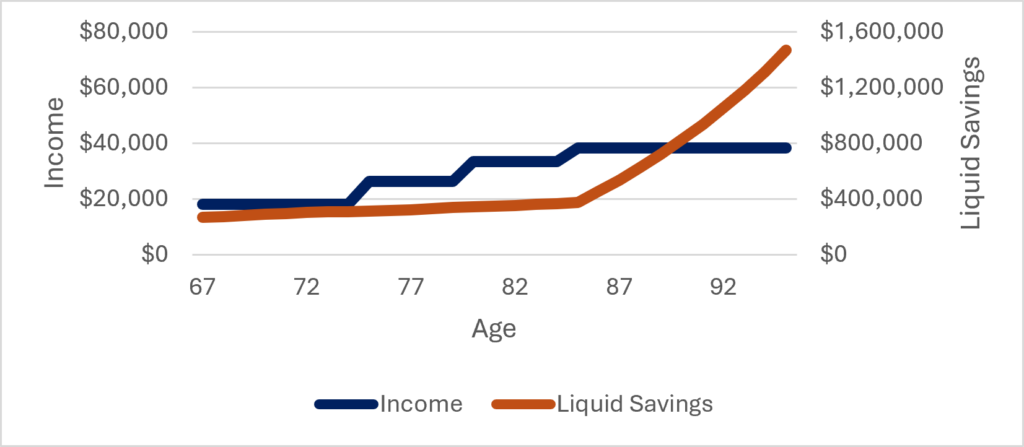

- Analyze standard configurations under HECM and QLAC and why they may not work for your retirement plan. The charts below demonstrate results from both HECM and QLAC on standalone basis as often presented to retirees.

HECM – Drawdowns and Liquid Savings QLAC – Lifetime Income (Defer to Age 85)

- Use a new algorithm for a combination of HECM and QLAC (HomeEquity2Income or H2I), to meet twin retiree objectives of (a) increasing income, and (b) increasing liquid savings. And at the same time, establish a building block for your retirement plan.

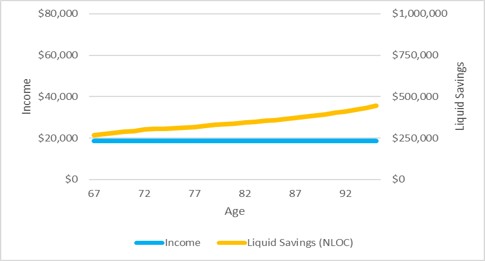

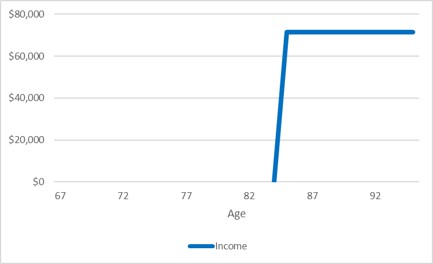

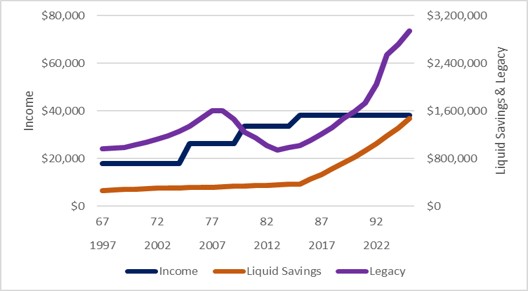

H2I: Combination of HECM and QLAC

Increasing Income and Liquid Savings

Total Income to 95: $850,000 Liquid Savings at 95: $1,450,000

Testing H2I for legacy and historical rates

While income and liquid savings are two important elements of H2I, retirees may also consider the effect of H2I on the legacy they’re providing to spouse and other family members.

Also, the broad message for planning is not to try to predict the exact amount of savings or legacy for each homeowner, but to demonstrate the possible impact of the market performance on your own plan. The illustrations above were based on industry standard fixed rates but, as covered in Treat Home Equity Like Other Investments, we believe it necessary to Illustrate benefits based on historical performance. By using historical rates, we are looking at the interplay of various product elements with real-world performance.

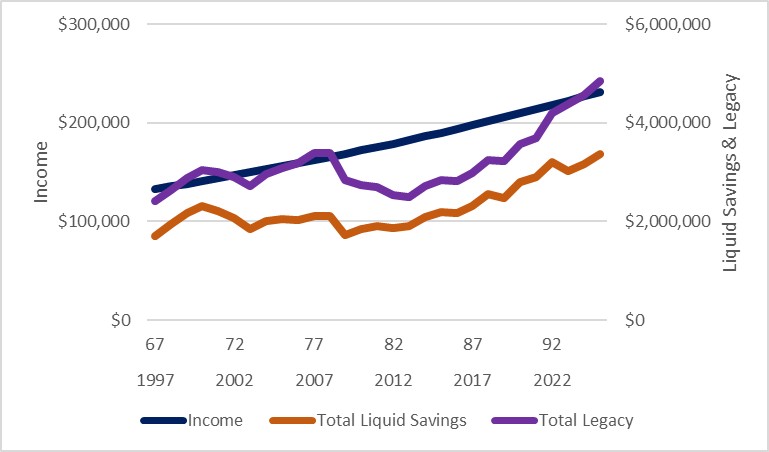

H2I: Combination of HECM and QLAC (Historical Rates)

Increasing Income, Liquid Savings and Legacy

Total Income to 95: $850,000 Liquid Savings at 95: $1,450,000 Legacy at 95: $2,950,000

Looking at the expanded example of this combination, here’s what we learned about each component:

- HECM’s liquid savings grow dramatically when you stop drawing down from line of credit and use a part of QLAC income to pay down the loan balance.

- QLAC may be purchased in a laddered format to create increasing income before age 85. In limited situations, QLAC income may be accelerated before its original income start age.

- And in combination, HECM and QLAC offer significant tax advantages, particularly in early retirement years.

Use H2I as a building block in a retirement plan with other savings

With H2I in place, the question becomes how we might further combine it with other retirement savings. Let’s look at adding to H2I our sample retiree’s Rollover IRA savings ($800,000 after QLAC premium), Personal Savings ($1 million) and Social Security payments ($36,000 starting at 67). While portfolio allocation is often a very personal decision, here’s what our starting plan reflects:

- Allocation of $800,000 in IRA: Stocks (growth) and Bonds in a Balanced Portfolio

- Allocation of $1 million in Personal Savings: Stock (high dividends), Bonds, SPIA

What is the starting income this plan will support? Using H2I as a building block and the Go2Income planning algorithm, the starting income is $133,000. The plan assumes that income will grow at 2% per year.

Go2Income -H2I, Rollover IRA, Personal Savings (Historical Rates)

Increasing Income, Liquid Savings, Legacy

Total Income to 95: $5,150,000- Liquid Savings at 95: $3,350,000- Legacy at 95: $4,850,000

With the $36,000 of Social Security benefits the total starting income is $169,000. The retiree can, of course, refine the plan to increase income and lower the substantial amounts of legacy and liquid savings.

Long-term care scenario testing

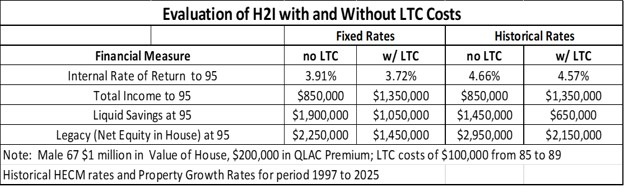

The next step in the process was to test various H2I scenarios as they related to covering long-term care. That’s particularly timely with greater longevity and increased responsibility of retirees, leading to coverage of more long-term care costs.

- The economic return for H2I in the 3.5% to 4.5% range is attractive recognizing the major asset is the housing wealth, assuming a growth rate around 4%. In one sense the higher crediting rate on QLAC is offsetting the higher HECM interest rate.

- In the scenarios above, we are able to generate additional income and cover $100,000 in LTC costs over five years from age 85 to 89. We would need to do some stress testing for larger or different patterns of LTC expense. Of course, we should consider the resources from other retirement savings.

- The income tax effects may be quite positive with all HECM drawdowns tax free, QLAC income deferred until received, and LTC costs being tax deductible. See The 9% Solution.

H2I for this sample investor can cover a reasonable amount of LTC costs while delivering higher income. The final planning steps include further testing to confirm results. Including a measure of income taxes, market risk and IRR before and after tax, we look at three qualities of the plan in our evaluation:

- Inflation protection

- After-tax income

- Stock market risk

For retirees, it means they no longer need to keep an eye on new caps for home equity, or spend down all their other assets to qualify for Medicaid’s LTC benefits. Even for those who never considered Medicaid as an option, H2I provides an easier way to create wealth from retirement savings while aging in place.

**********************************************************************************

Unlike product innovation in the past, these design changes don’t require regulatory change, product pricing or design changes, or special servicing. Just stack these building blocks and assemble them as the plan instructs. Visit Go2Income, where you can start building your own plan.