There’s a lot of promotion of ‘alternative investments’ these days, from gold to real estate and even to Bitcoin.

Are you missing out?

If you do any research on your own about how to create a solid retirement, you’ve read about alternative investments, financial managers who boast great performance and the tech stock your friends cashed in on.

You’re also seeing that your kids could use your help with the down payment on a house or condo with more space.

Can you afford to make that riskier investment or help your kids — without jeopardizing your own retirement plans?

Your plan for retirement income

Before you make a decision about whether alternative investments would work, you need to understand whether you have a retirement plan set up with the foundational building blocks:

- Investment portfolios that are traded, have a daily market value, have low fees and must pay out distributions under proscribed regulations

- Income annuities that are issued by highly rated insurance companies that either pay out guaranteed lifetime income or can be exchanged to contracts that do

- Equity in the value of your house that can be extracted without risk to the homeowner

As we’ve reported in previous Kiplinger.com articles, we take a pretty conservative approach to constructing your plan for retirement income. For example, in How to Get More Retirement Income From Your 401(k), I wrote about making conservative assumptions about long-term market performance and creating “an integrated approach with both investments and annuities that provides more income and protection against inflation and late-in-life expenses.”

Now, about the “outside the plan” investments.

What are alternative investments?

I asked ChatGPT about the investments that might be considered “alternative.” Here’s AI’s list:

- Investment real estate

- Private equity and hedge funds

- Commodities

- Gold, other precious metals and collectibles

- Peer-to-peer lending

- Farmland and timberland

- Green energy and sustainable investments

By the way, cryptocurrency was not on the list. If AI didn’t include it, that’s good enough for me.

Well-read DIY investors understand the upside and downside of most of these, but let’s go over some of AI’s thinking:

Pros for alternative investments:

- Diversification. Alternatives can provide diversification benefits because they often have low correlations with traditional asset classes like stocks and bonds. This can help spread risk and reduce the impact of market volatility.

- Potentially higher returns. Some alternative investments, such as private equity and hedge funds, have the potential to deliver higher returns than traditional investments over the long term.

- Portfolio customization and risk management. Alternatives allow investors to tailor their portfolios to specific goals or preferences, whether it’s ethical investing, impact investing or a focus on a particular sector. And certain alternatives, like real estate and commodities, can act as hedges against inflation and provide stability during economic downturns.

Cons for alternative investments:

- Lack of liquidity. Some alternative investments, such as private equity or certain real estate investments, are illiquid, making it difficult to access your funds on short notice.

- Higher risk. Alternative investments can be riskier than traditional assets. Strategies like leveraged investments or investments in startups can result in significant losses.

- Tax and regulatory complexity. Regulations and tax treatment for alternative investments can be complicated and vary by jurisdiction, potentially leading to unexpected tax liabilities or compliance challenges.

Intrafamily loans or advances

While ChatGPT did a good job of identifying and critiquing alternative investments, many of us are exposed to other, more personal investments that also limit our choices and opportunities for due diligence. That may happen when the kids ask about providing the down payment on their first or even second house.

The intrafamily loans offer an interest rate, but you cross your fingers that you’ll get paid back. Or the kids, again, have some property where they could build or renovate and generate some rental income. Finally, with college costs continuing to soar, you may need to fund that 529 plan at an even higher rate.

You’d like to be available, but also get a decent return, and your money back.

More aggressive stock and bond investments

Another approach may come from a neighbor or broker who brags about the great return on some investment they got, typically by taking more investment risk. Here are two examples:

Small cap stocks. These investments in smaller, often early-stage companies, are volatile because the firms have fewer resources if they get into financial trouble and are more likely to fail. But when one succeeds, its stock can flourish. Fidelity reports that now might be a good time to invest because, “Small caps were recently trading at substantial and attractive discounts relative to large-company stocks, and could be due for a stretch of outperformance.” At the same time, NerdWallet points out that “as small-cap businesses expand, their stocks offer a higher growth potential compared with larger companies. But that comes with a greater risk of volatility — including more (and bigger) fluctuations in stock prices and earnings reports.”

High-yield bonds. It’s easy to find companies offering “to help investors navigate today’s income problem,” with high-yield bond funds, some of which offer annual returns of 9% to 12%. You can also easily find this description from Morningstar, which discusses risk: “High-yield bond portfolios concentrate on lower-quality bonds, which are riskier than those of higher-quality companies. These portfolios generally offer higher yields than other types of portfolios, but they are also more vulnerable to economic and credit risk. They primarily invest in U.S. high-income debt securities where at least 65% or more of bond assets are not rated or are rated by a major agency such as Standard & Poor’s or Moody’s at the level of BB (considered speculative for taxable bonds) and below.”

Should retirees consider? If so, in what circumstances?

As I said above, I think you should consider higher-risk investments only when your plan for retirement income is safe. Here are my criteria for a safe plan:

- You need an income stream that will cover your expenses now and in the future. Money that will be deposited in your bank account every month without question. And, of course, income that is paid for life.

- Keep an eye on inflation. Happily, Social Security is indexed for inflation, but most other financial products are not. If you have a solid retirement plan, however — one featuring a portfolio of income annuities and a reasonable amount of stocks/bonds that deliver dividends and interest, along with the potential for growth — you can protect yourself against reasonable long-term rates of inflation.

- Most retirees hope to leave a legacy to family or favored charities, which can be built into your plan. That’s an area where personal objectives vary, but whatever your plan, it should be designed to meet that objective.

- Liquidity is money that you may need in case of unplanned expenses. It can be used to pay for unreimbursed long-term care or health care costs that you can pretty much count on experiencing at some point.

How to free up funds for alternative investments

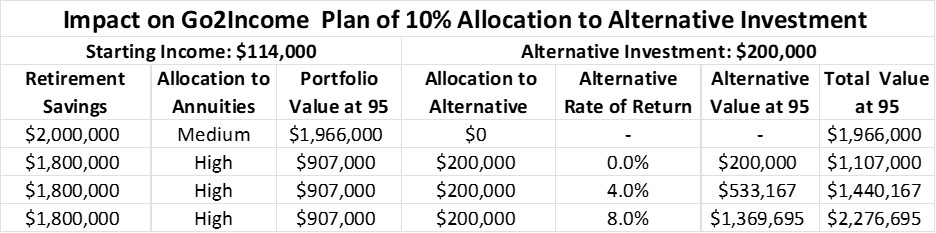

If you have all that under control, yes, you may consider the “outside the plan” investments. Here are examples of freeing up 10%, or $200,000, in our sample investor’s plan, for these investments — while still keeping the plan safe. The Go2Income tool does that in this case in two ways: by increasing the allocation to annuities and by making additional IRA withdrawals. It’s doable, but it’s a highly personal call, impacting the portfolio value late in retirement for both legacy and liquidity.

Note how the return on the alternative investment determines whether it was a profitable decision.

Take your time to make this decision

Investing in alternative investments requires lots of research as well as the nerves to do something most other retirees aren’t considering. You probably also need time to save up the money that you can invest without worrying about losses. But the sector does offer unique opportunities that may pay off when everything else is crashing.

To find out whether you can build a plan that allows you to experiment with alternative investments, visit Go2Income and answer a few questions. You may not end up making unusual investments, but you will have a plan that can guide you in retirement.