Combining IRA investments, lifetime income annuities and a HECM into a plan we call IRA4Income could significantly increase your retirement income and liquid savings compared to traditional planning.

You’ve worked hard to save for retirement in your 401(k) and now IRA — and succeeded. But wait. Your work isn’t done.

If you adopt a plan that combines assets to the best effect, our new IRA study shows average starting income of an IRA4Income plan of 50% to 75% over traditional planning.

Before describing the planning methodology and our study of the results, let’s describe these assets and answer the question, “Why haven’t I heard about this before?”

What are these assets? And why haven’t we seen this before?

Are we talking about high-yield bonds, complex annuities or other exotic investments? Nope. In fact, the elements are a little boring:

- An IRA account invested 50/50 in fixed income and stock investments

- Lifetime income annuities with income starting immediately or in the future

- A home equity conversion mortgage (HECM) that generates income and liquidity

What’s unique is that the asset classes come from three separate financial businesses — investments, insurance and mortgages — and the Go2Income planning methodology (a little like AI) has figured out how to put the pieces together for maximum benefit, for all retirement ages and objectives.

If you haven’t heard about this method, it’s because the different businesses operate quite separately, sales forces have their own requirements for what they can sell you, and combining these asset classes requires complying with multiple regulations.

That means most advisers can’t, or won’t, talk about the asset classes they don’t represent.

Consumers don’t share those restrictions and can explore something like my company’s IRA4Income method, which, besides the huge increase in income, creates more liquidity than the IRA alone. By age 85, it can provide nearly double the IRA by itself.

That increase could help to cover, for example, the long-term care costs that 40% of retirees will incur.

How well do these assets have to perform?

Using our Go2Income planning technology, we’ve put the assets together into IRA4Income by first combining two programs: IRA2Income, made up of investments and immediate annuities, and HomeEquity2Income, made up of a HECM and a QLAC deferred-income annuity. (For more on this combo, see my article How Combining your Home Equity and IRA Can Supercharge Your Retirement.)

As you’ll see below, these programs can also be set up on their own to provide benefits, even if you don’t seek the maximum win-win of complete integration into your retirement income plan.

Our study analyzes results for different ages, marital status, IRA savings amounts, value of home and market conditions.

The old rule about taking $40,000 as starting income from your $1 million IRA has been upended, with starting income amounts that range from $60,000 to $80,000, depending on the case.

Highlights from the study

Each case study starts with $1 million from a rollover IRA and $1 million in home value. Besides starting income, the study looks at liquid savings and legacy, making sure we consider all three key retirement objectives. Starting income grows by 1.5% per year until age 85.

Set out below are key results for sample cases, as well as key planning assumptions:

62-year-old man

Starting income: $70,000

Total liquid savings at 85: $763,000

Total legacy at 95: $2,597,000

65-year-old woman

Starting income: $69,100

Total liquid savings at 85: $977,000

Total legacy at 95: $2,659,000

70-year-old couple

Starting income: $68,200

Total liquid savings at 85: $1,138,000

Total legacy at 95: $2,583,000

75-year-old couple

Starting income: $70,700

Total liquid savings at 85: $1,115,000

Total legacy at 95: $2,364,000

Key planning assumptions:

Investment Returns: Stock Market Return: 8%; Fixed Income Total Return: 5%

Allocation to Annuities: Immediate Annuity: 30%; QLAC Deferred Income Annuity: 20%

HECM: Adjustable Interest Rate: 7.75%

Too good to be true?

As with any retirement plan, the study results are based on certain assumptions about the performance of each asset class. The most important aspect is that no one assumption drives the results:

- The lifetime annuity is fully guaranteed and is issued by a highly rated insurance company

- The HECM interest rates are adjustable within limits, but with a large portion of the mortgage interest paid by the QLAC deferred-income annuity

- The IRA investment assumptions reflect an equity return that is lower than average long-term market returns

In setting up a personalized plan, you can customize the assumptions to your risk tolerance.

An IRA4Income plan in more detail

Let’s look at our example investor, Sally, age 70, who now has $1 million in rollover IRA savings and a home worth the same amount. She wants the maximum amount of income, within reason, and liquidity for long-term care costs.

Fortunately, Sally has read our articles and realizes her home is a valuable asset and that she can consider it as a way to ensure her money not only lasts for her lifetime but also provides a resource for unplanned expenses.

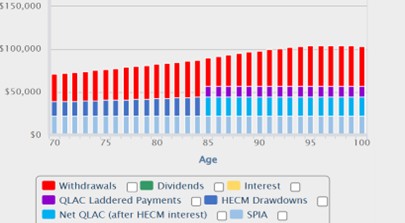

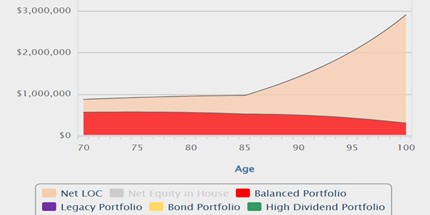

The charts below demonstrate how IRA4Income can bolster her spendable income (starting at $71,000) while providing access to savings that could pay for large unplanned expenses after age 85. Her total liquid savings under this plan are nearly $1 million at age 85 and will continue to grow thereafter.

Sources of income

Liquid savings

What about taxes? What about risk?

Sally is not obsessed with taxes but would like to understand whether there’s any portion of her income, unlike the IRA, that’s free from tax. She’s pleased that, until 85, about 20% of her income is tax-free.

If we measure risk by the uncertainty of the value of the investment portfolio, a 100% IRA is all at risk, while with IRA4Income, only about 50% is subject to market risk.

If you’re nervous about plunging in all at once, the parts of an IRA4Income plan can be put in place one at a time, following your own timeline.

As pointed out above, you could start by combining investments with an immediate income annuity (IRA2Income) or access the value of your home with a HECM and a QLAC.

At the same time, you might consider whether to delay claiming your Social Security benefits to get larger payments.

You might be able to wait until 73 (or 75 if you were born in 1960 or later) to take RMDs (required minimum distributions) from an IRA, allowing that income source to grow.

When you consider all your options together, you have choices.

Are you ready to start now?

In these articles, we have worked to explain these financial approaches in clear language so readers can talk knowledgeably with an adviser about what steps to take and when.

Still, there are indications that some people just throw their hands in the air and resolve to live with their savings in different silos for stocks/bonds, annuities and their home.

You don’t have to do that.

————————————–

Instead, visit Go2Income to order a Go2Income plan that with IRA4Income inside can meet more of your retirement objectives. A Go2Specialist can answer questions about the plan or refer you to a qualified adviser.