An integrated approach of investments and annuities could provide you with more retirement income in addition to protection against inflation and late-in-life expenses.

One might yearn for the days of company pensions, but we live in the era of the 401(k) and similar plans, so we might as well take full advantage of them. That means socking away at least the maximum that your plan provides in pre-tax contributions and encouraging your bosses to offer matching payments and the investments that will best help grow your pot of retirement money.

In fact, at least 85% of all eligible employers offer a 401(k) and employees put an average of 6.5% of their salaries into them each year. According to a report by Fidelity, the average 401(k) balance reached $112,400 in the second quarter of this year.

All good news!

Current options from your employer or AI

When you are ready to leave that job, however, things change. Very few, and particularly small businesses, employer-sponsored programs offer a retirement planning option. The most guidance you might get is something like, “You can stay invested in our investment portfolios and hope they produce regular income like your career did, or maybe you can invest your savings in an income annuity and enjoy the income safety annuities offer.”

Or, you might ask a chatbot like ChatGPT for advice. We asked, “How much income can I expect from the $1 million I have in my 401(k) plan when I take late retirement at age 70?” The answer was a generic recommendation to withdraw 4% a year for as long as you can.

None of those is a good enough alternative

If you stay wholly invested in the markets, you’ll need to withdraw your income from your savings, which is not the same as getting employer matches and reinvesting investment earnings, and taking advantage of dollar-cost averaging when the markets go down. (After retirement, when the markets dive, there’s no silver lining.) Remember that average investors on their own underperform the market by 1% to 2% per year.

Putting all your money into an income annuity is indeed safe, but may not get adequate inflation protection or have liquid funds for expenses like medical and caregiver costs. Even if your employer does suggest annuity choices, you should ask whether they are based on current rates in the market and offer a choice of competitive carriers.

And the 4% rule has been discredited by experts, particularly its performance in 2022 when both the bond and stock markets fell.

There is a better way, an integrated approach with both investments and annuities that provides more income and protection against inflation and late-in-life expenses, as well as a starting income percentage of more than 6% for some plans.

Use your qualified plan savings for income

I wrote in my recent article Do You Have Enough Money to Retire? That Is the Question that retirees should “focus on retirement income, but don’t lose sight of other considerations, like legacy and liquidity. Most important, wherever possible, test whether a particular product or strategy improves your income and other objectives.”

To illustrate, let’s examine two scenarios under IRA2Income planning for a 70-year-old female who has $1 million in her qualified savings accounts.

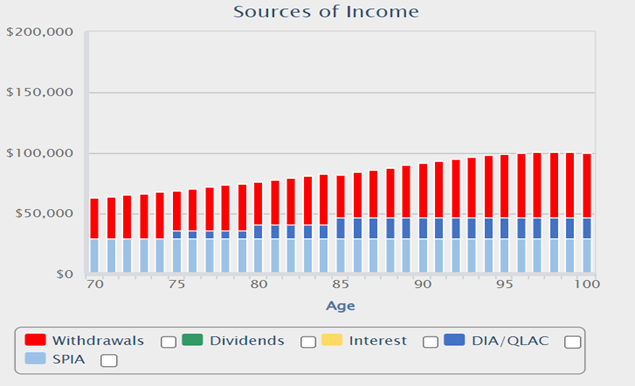

1. Maximize current income. In this scenario, our retiree will invest all of her savings in a balanced portfolio of stock and bond investments and two types of income annuities. Those annuities, in turn, will be split between (1) an immediate annuity with income starting at age 70 and (2) a deferred income annuity called a QLAC providing laddered income to protect against inflation.

You may remember news about the QLAC, or qualifying longevity annuity contract, from last year, when Congress enacted the SECURE 2.0 Act. A QLAC allows you to defer more taxes and buy more retirement income from your 401(k), rollover IRA or similar tax-qualified accounts. Despite the favorable legislation, not all employer-based planning integrates QLACs into their solutions.

Under this plan, pictured below, our retiree’s starting income is $62,700, or 6.27% of her savings. A far cry from 4%.

The value of her legacy at 95 will still be nearly $500,000 at age 95, despite having to meet RMD requirements. If she wants to leave a larger legacy for the grandkids, she can try to build up her personal savings. And her portfolio from qualified plan savings at age 95 is higher than it might have been because, with the guaranteed income from the annuities, she was able to take a little more risk on the withdrawals from her balanced portfolio allocation.

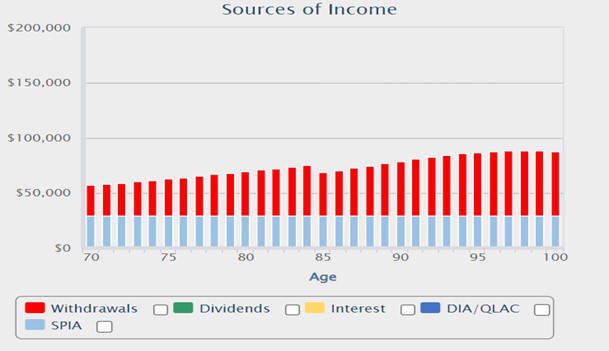

2. Build a cushion for late-in-retirement expenses. In this scenario, our investor puts $100,000 of her $1 million of savings in a QLAC that will provide payments of $25,000 per year at age 85. She is looking ahead to health care insurance premiums and costs that may kick in with home aides, procedures or hospitalization.

Her starting income under this plan, from the $900,000 that remains in savings at 70, will be $57,063.

Even after 25 years of taking payments from the investments she built up as she saved for retirement, her legacy will amount to $509,000. Of course, she’ll also have the $25,000 per year from the QLAC.

These are just two of the many options that you can design for yourself. There’s even one more on the Go2Income drawing board, particularly for younger new retires who like the safety of these plans but don’t want to pay taxes before RMDs are required. (Contact me if you’d like to discuss this feature.)

Part of your total plan

For all the good that your 401(k), IRA and similar products can do for your retirement, they aren’t the only consideration. You will likely also have personal savings, Social Security and possibly a pension that will all add to your income potential. You can look at each separately (with IRA2Income and Savings2Income, for example) or integrate all income sources into an overall Go2Income plan based on your specific circumstances and needs, including how to find the best annuity provider among the highest-rated insurance companies. Those are all benefits you won’t get from your former employer or artificial intelligence.

To try out a plan, visit Go2Income, answer a few simple questions and get started on a plan to create maximum income from your savings.