It’s come to the point in your life when retirement is on the horizon. Most investors find themselves in one of two situations when they get here:

- Based on your savings and current retirement strategy, you are confident that when that time comes to say goodbye to the workforce and hello to a new stage in your life you’ll have the security of regular income.

OR

- Based on the choices you’ve made throughout the years of working and investing, you are unsure that you’re ready, making retirement a daunting task.

If you are reading this blog, I’ll assume you understand the fundamentals of QLAC. Even with that knowledge though there are still advantages these products offer that average investors, and even advisors, don’t understand.

Since I came across a comment the other day criticizing QLAC for not providing protection against inflation, let’s focus in this post on how QLACs can provide increasing income throughout retirement.

Inflation protection is a challenge hurled at many financial products, but in reality what investments, other than TIPS (Treasury Inflation-Protected Securities) bonds, do provide that protection? It’s unfair to point out this lack in QLACs without also acknowledging that most investment vehicles don’t offer this ability.

There are some things an investor can do with a QLAC though to create increasing income. Here are just a few:

- Purchase a QLAC with increasing income payments. Pacific Life, Lincoln Financial, & American General are among QLAC issuers that have this feature.

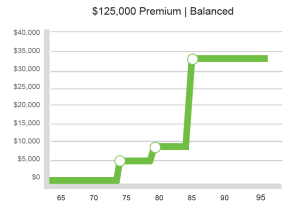

Ladder QLAC purchases over time. Knowing that QLAC has a $125,000 premium limit, one could purchase $25,000 per year every three years, say, from age 65 to 77, each time increasing the longevity protection.

Ladder QLAC purchases over time. Knowing that QLAC has a $125,000 premium limit, one could purchase $25,000 per year every three years, say, from age 65 to 77, each time increasing the longevity protection.- Purchase a QLAC in a lump sum with different Income Start Age To get the maximum tax benefit and to create increasing income, an investor could specify ISAs of 75, 80 and 85. Set out below is an example of how that might work.

Of course, the above approaches could be supplemented with additional purchases as the QLAC limits are increased, either because (1) the 25% limit increases because of market value increases in the investment portfolio or (2) the $125,000 limit increases because of inflation.

The use of longevity annuity contracts in IRAs and tax-qualified defined contribution plans is quickly becoming a big part of the retirement landscape, redefining the annuity and putting the power back in the investor’s hands.

Knowledge is power. Therefore, I strongly urge you to learn more about QLACs and how you can customize your retirement strategy to provide maximum, increasing income.

And when you’re ready to find a QLAC that’s right for you, visit my Go2Income Toolkit. It will identify the best QLAC for you based on your specific needs and circumstances.

9 retirement planning trends that make us thankful this season

[…] while maintaining its safety and unique role as a source of guaranteed lifetime income. QLAC, for instance, is a good example of a new use of deferred income annuities that enables consumers […]

8 Financial Conversation Starters for Thanksgiving Table Talk | Day Traders Finance

[…] while maintaining its safety and unique role as a source of guaranteed lifetime income. The QLAC, for instance, is a good example of a new use of deferred income annuities that enables consumers to create […]

8 Financial Conversation Starters for Thanksgiving Table Talk | Investing Daily News

[…] while maintaining its safety and unique role as a source of guaranteed lifetime income. The QLAC, for instance, is a good example of a new use of deferred income annuities that enables consumers to create […]

Financial independence means having a plan for retirement income

[…] form of deferred income annuity called a “QLAC” or “Qualifying Longevity Annuity Contract” is purchased with rollover IRA […]