A lot of retirement guidance I have read lately continues to treat baby boomers the same as the rest of the investor public. Even after the first six months of 2022, when the traditional 60/40 stock/bond portfolio sank more than 20%.

I may not dispute the traditional approach for investors who are 25, 35 or 45 years old and accumulating savings for retirement or the kids’ college education. As we know, markets historically rebound, and younger investors with time to recover from market corrections have the benefit of dollar cost averaging.

But boomers entering or in retirement have different needs than all the “Gens” that have come after them: they may not be able to wait around for their depressed accounts to grow again. For boomers, income is the important consideration — income that stays steady and grows over the decades of retirement.

Where to find income

Economic downturns always provide winners along with the many losers, and annuity payment contracts (also called income annuities) — which with rising interest rates have increased the payouts on new contracts — are the current winners. As of August 15, 2022, new purchases of income annuities at certain ages are providing 20% to 50% (depending on the income start age) more than at the beginning of the year, and that could go up even further. (They’re almost the mirror image of mortgage interest rates, which are also going up.)

How much do you think a 20% increase in annuity payments is worth? Just imagine that your starting Social Security benefit you could claim next year went up from $3,000 to $3,600 per month. Would that get your attention?

Yet, most financial pundits are still talking only about investment assets, not about income. Maybe because it’s easier — not because it’s better — to lump in these boomers with everyone else.

Another Type of Allocation is Needed for a Retirement Income Plan

While a 60% stock/40% bond allocation may not be appropriate for boomers, a different type of 60/40 allocation may be: one that includes a mixture of stocks and bonds along with Income annuities. We call that a Go2Income plan.

When you build that Go2Income plan for retirement income, you may start with 60% of your retirement savings in investment portfolios and 40% in income annuities. But that allocation is different than the 60/40 referred to above.

- It is based on output and not input, and in a Go2Income plan you might end up with splits of 67/33, 75/25 or another allocation.

- The split will change over time, with an increasing allocation to income annuities — to assure lifetime income.

- Most importantly, the split is designed to meet your personal objectives and priorities and not your neighbors.

We’ve talked about the allocation among types of annuity payments (see For Sustainable Retirement Income, You Need These 5 Building Blocks). So, let’s talk about the allocation within the investment portion.

Allocation of Investment Portion of Go2Income Plan

A Go2Income plan will use a share of the investment portion of your retirement savings to be a source of safe income rather than strictly as a source of capital growth.

In the Go2Income strategy there are three types of portfolios:

- High Dividend Portfolio: This is primarily a source of increasing tax-advantaged income plus growth of capital and is invested in an account with after-tax or non-qualified savings.

- Fixed Income Portfolio: A source of fixed income plus general safety of capital, replaced in part by guaranteed annuity payments. It will be invested in your non-qualified retirement savings account.

- Balanced Portfolio: A source of withdrawals of capital from your rollover IRA account to achieve increasing income and at the same time meet RMDs. This will be a blend of a growth portfolio and a fixed income portfolio to reduce withdrawal risk.

The allocation to stocks within the investment portfolios can be high, medium and low but you should consider what percentage your stocks take up in your overall portfolio. A high allocation of stocks within the 60% in investment portfolios may often be selected when a high allocation to income annuities is chosen within the 40% portion. The overall impact of these two elections is a higher allocation to fixed income assets, primarily in annuities.

Tactical Allocation within Each Portfolio

The tactical implementation of the investment portfolios within a Go2Income plan must address (1) whether you use an outside adviser or set up a self-directed investment account, (2) the types of investments (ETF, mutual fund or individual securities), and (3) the allocation to specific sectors of the market.

We start with the premise that you want to achieve your income objectives, with low fees and low planning risk, while achieving your legacy objectives. We add in easy plan monitoring and plan management so you might be able to manage portfolios on your own. In any event, working out a personal Go2Income plan will help a do-it-yourselfer decide what questions to ask an adviser.

Some investors may research and buy individual stocks and bonds in these portfolios, but there are other options for the investment portion of a retirement income plan that are perhaps easier to manage and understand, including mutual funds and ETFs

Portfolios Designed Specifically for Go2Income

In addition to mutual funds and ETFs for the investment portfolios, there are other pooled investments that can be targeted to a specific objective and managed with the help of artificial intelligence (AI) tools. We decided to explore that option for Go2Income.

We consulted with a company, FolioBeyond, which is a “quantamental” manager using advanced algorithms, including artificial intelligence (AI) tools, to construct portfolios. Quantamental investors employ quantitative methods, tools and technologies to make investment choices.

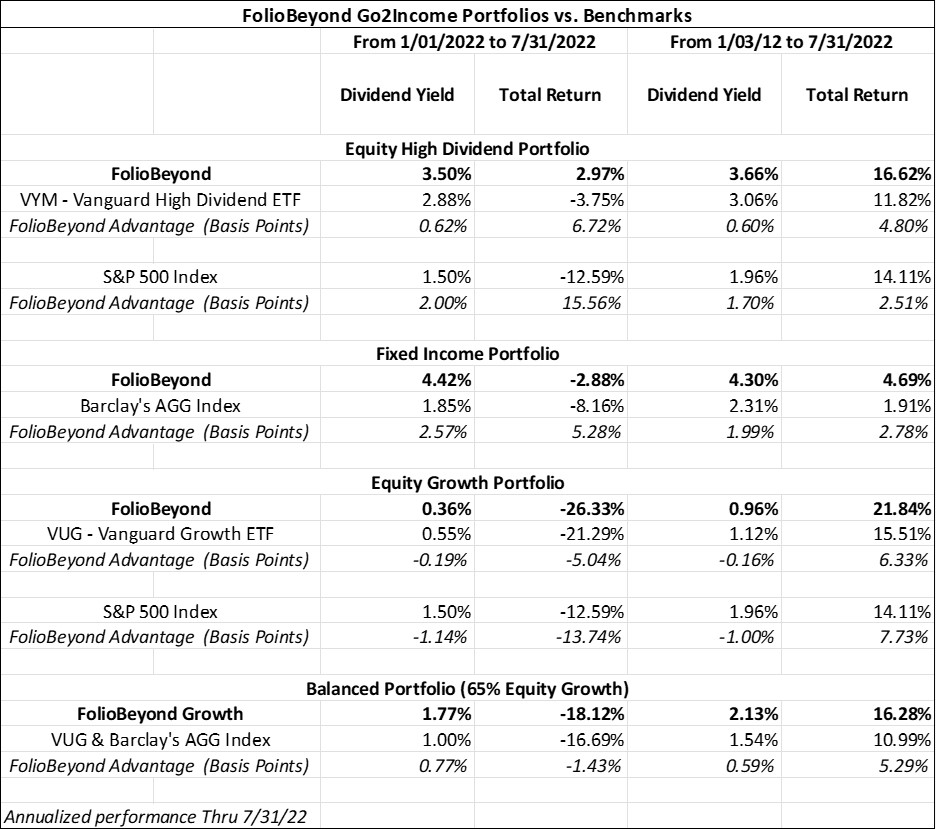

FolioBeyond was asked to design the high-dividend, fixed-income and balanced portfolios to align with Go2Income planning. The objectives of each portfolio were to match the interest and dividend yields of comparable low-cost ETFs and to outperform those ETFs on a total return basis by 1% to 2% per year. We also wanted them to keep fees low.

Set out below are back-tested investment results of these portfolios vs. benchmark indices for the first seven months of 2022, and the 10 1/2 years since 2012. The FolioBeyond portfolios exceeded both yields and total returns of comparable benchmarks (see “FolioBeyond Advantage”) in most scenarios. Of course, back-tested results are achieved while knowing what occurred in past markets and can’t be used to predict future performance. See the discussion below chart for other caveats.

The return performance shown above is based on back-tested simulations prior to February 2021 for the equity model and November 2020 for the fixed income model. Actual performance for client accounts may be materially lower than that of the modeled portfolios.

Back-tested performance:

- Does not represent actual performance and should not be interpreted as an indication of such performance. Such results do not represent the impact that material economic and market factors might have on an investment adviser’s decision-making process if the adviser were actually managing client money.

- Differs from actual performance because it is achieved through the retroactive application of model portfolios designed with the benefit of hindsight.

- Could be either favorable or unfavorable if portfolio models are changed from time to time.

Three Take-aways from this Article

- Allocating for retirement income is different than allocating for accumulating retirement savings.

- Allocating the investment portion of a retirement income plan to specific portfolios must align with income goals and how income is sourced.

- There are lots of options for managing individual portfolios but make sure to look at both yields and returns net of fees and how each impacts your plan.

If you are interested in creating a plan for retirement income that reflects your specific needs, visit Go2Income for a complimentary personalized plan that delivers both a high starting income and growing lifetime income, as well as long-term savings.