How the right plan now can get you back on track and reduce the risk going forward

You know what they say about the best laid plans going awry. Well, with what has been going on in the financial world this year, that’s what has happened to countless retirement plans.

For instance, let’s look at one hypothetical retiree who, until recently, thought she was all set. Our sample investor put off formalizing her plan for retirement income until she began taking Social Security at age 70 and making withdrawals from her rollover IRA. It was December of 2021. Inflation seemed to be reasonably under control; the markets were performing well; and with 50% of her $2 million portfolio invested in bonds it was pretty conservative.

Social Security and a pension totaling $60,000 per year helped her meet her starting income goal of $150,000. The balance of $90,000 was coming from her $2 million in retirement savings.

Even after having to draw down part of her personal savings to make her income goal, she also was leaving a solid legacy, assuming historical market returns. She used a traditional income planning approach relying only on her investments. She was fine and felt reasonably secure.

As with many like her, including financial pundits, she didn’t anticipate market gyrations for anything like what happened next.

What happened during the first 6 months of 2022?

Sometimes the consequence of market volatility is that you simply have to cut back in your spending during unanticipated rocky patches. The same could happen to you after retirement if your plan doesn’t account for real-life possibilities. So, here’s what has happened so far in 2022.

- First, inflation hit, rising over 8%. A recent survey found that in response to higher inflation, 35% of people planning for retirement are cutting back on social activities, and 28% are spending less on travel in order to maintain or increase their retirement contributions. Our investor wasn’t ready to make radical changes to her lifestyle.

- Second, because of market drops, the portion of her investment portfolios in growth stocks fell over 30% since the beginning of 2022. (The portion in high-dividend stocks held up for a while but ended up falling over 8%.)

- Third, the value of her fixed income portfolio fell by around 14%, reducing both her rollover IRA and personal savings accounts. She definitely wasn’t prepared for that.

- Fourth, the combined effect was that the savings she was using to draw down income (rollover IRA plus part of personal savings) were down over 20%. Her bonds didn’t protect her.

What did these developments do to her plan for retirement income?

A lot of individuals become shy at times like these and won’t even discuss what the long-term results might do to their plan, but our investor wanted to fully update her plan to current market conditions. Here is what she discovered.

As she looked at inflation, our investor figured her living expenses were up $10,000 per year, bringing her income goal to $160,000. (She did believe that there might be a lower rate of inflation going forward.) Her Social Security and pension will still contribute $60,000 a year (good for that) so her retirement goal from savings is now $100,000.

With her retirement savings down below $1.6 million, using the previous strategy will produce only $74,000 per year as her starting income — $26,000 short of her new budget. If she believes in a lower rate of inflation going forward, say 1%, her plan income would be $82,000 — still $18,000 short. Drawing down more of her savings to make up this shortfall reduces her legacy and even increases the risk of running out of money.

Let’s turn back the clock and see how a Go2Income plan would have fared instead.

What you can get from a Go2Income plan

The key differences between Go2Income and traditional income planning are:

- Annuity payments as a source of income.

- Lower allocation to stocks overall but with a higher allocation to high-dividend stocks.

- An algorithm that integrates all sources of income.

So, let’s see how this plan would have worked.

Her starting income from savings in December 2021 would have been over $100,000, giving her a $10,000 cushion against her original $90,000 from savings. And because of annuity payments in the mix, more of the income would be safe and less would be taxable.

At the end of June 2022 with the different allocation to stocks under the Go2Income plan, the value of her invested savings would have fallen $245,000 vs. $400,000 under a traditional plan. Her income under an updated plan supported by the lower savings has fallen, but only to $91,000.

To meet her new goal of $100,000 from savings she’s willing to assume a lower inflation rate of 1%, figuring she can gradually adjust, and her new income is $100,000 – bringing the total back above $160,000.

Of course, she can’t go back in time.

Converting her traditional plan to a Go2Income Plan?

While kicking herself about not adopting Go2Income earlier, she doesn’t want to compound her problems. So, what would a new Go2Income plan look like starting with the $1.6 million from the original plan? She was pleasantly surprised to find out she would still be OK. The reasons why include those stated above, plus one more — annuities are even more attractive now because of an increase in interest rates.

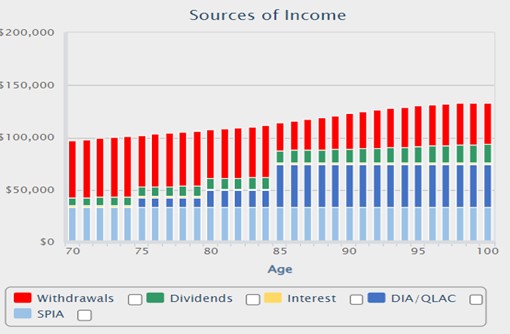

Without any change in assumptions, her income under a new Go2Income plan as of June 30, 2022, would be $88,000, even starting with savings under $1.6 million; if she lowers her inflation expectation to 1% per year her income is back to $97,000. Here’s a picture of her new plan.

In thinking about making a change in her planning method, she should make sure that where possible she considers the tax consequences of such a move. She can, of course, stay with her current investment advisers or manage the money herself if she prefers.

It was a very tough six months — and it might continue. She is thankful that she could make her retirement plans more secure.

Final thoughts

Ever the thoughtful investor, she asked whether the annuity rates might go up even further in the future. While that’s highly likely there is a risk of delay, lower cash flow, greater risk exposure and worse tax treatment. The smart compromise may be to implement the immediate annuity payments now and delay future annuity payments.

By the way, she shouldn’t scold herself too much for not adopting a Go2Income plan earlier. While there was an economic loss to having delayed, the real loss was a loss of sleep. As we’ve said, Go2Income is built to deliver a more secure retirement.

We can help if you have a similar situation. Visit Go2Income for a complimentary personalized plan that delivers both a high starting income and growing lifetime income, as well as long-term savings.